Last Update : 09/04/2026

Agar aaj aapki income band ho jaye to kal kya hoga? Ye sawal simple lagta hai, lekin maximum log isse avoid karte hain. Reality ye hai ki India me majority log retirement ke baad financially dependent ho jate hain kyunki unhone planning hi nahi ki hoti.

Yahin par Atal Pension Yojana (APY) ek silent solution ke roop me aati hai. Lekin twist ye hai ki log ise ya to ignore kar dete hain ya galat samajh lete hain. Sach ye hai ki APY powerful hai, lekin sirf tab jab aap ise sahi tarike se use kare.

Atal Pension Yojana ek government-backed pension scheme hai jo specially un logon ke liye design ki gayi hai jo organized sector me nahi hai. Isme aap monthly chhota contribution karke future me ₹1000 se ₹5000 tak guaranteed pension pa sakte hai.

Ayushman card 2026 Me kaise Banaye…. Click Here

APY Scheme ka Objective kya hai

Is scheme ka main goal hai ki har citizen ko retirement ke baad financial security mile. India me kaafi log aise hain jinke paas pension ka koi system nahi hota. APY isi gap ko fill karta hai.

Government chahti hai ki log early age se savings start karein aur retirement ke time unhe fixed monthly income mile. Ye ek tarah se future ke liye safety net hai.

Ye scheme kiske liye banayi gayi hai

APY specially low-income aur unorganized sector workers ke liye banayi gayi hai. Jaise daily wage workers, small shopkeepers, drivers, etc.

Lekin aaj kal middle class bhi is scheme me interest le raha hai. Kyunki ye simple, low-risk aur long-term secure option hai.

Govt guarantee ka kya matlab hai

Is scheme me sabse bada factor hai “guaranteed pension”. Matlab aapko retirement ke baad fixed amount milna hi milna hai.

Ye guarantee government deti hai isliye risk almost zero hota hai. Ye cheez APY ko baaki investment options se alag banati hai.

Atal Pension Yojana Kya Hai Overview

| Point | Details (Short) |

| Scheme Name | Atal Pension Yojana (APY) |

| Pension Range | ₹1000 – ₹5000 per month |

| Risk Level | Zero risk (Govt. guaranteed) |

| Best For | Low & middle income users |

| Strategy | APY + NPS/PPF combo best |

Atal Pension Yojana Eligibility Criteria

APY join karna easy lagta hai, lekin yahan bhi log basic mistakes kar dete hain. Agar aap eligibility properly check nahi karte, to aapka account reject ya inactive ho sakta hai.

Minimum aur maximum age limit

- Minimum age: 18 saal

- Maximum age: 40 saal

Delay karna sabse mehenga decision hota hai — late entry ka matlab same benefit ke liye zyada paisa.

Bank account aur Aadhaar requirement

- Active bank account mandatory

- Aadhaar linked hona chahiye

- Mobile number connected hona better

Auto-debit system fail hua to poora plan disrupt ho sakta hai.

Kaun log apply nahi kar sakte

- Income tax payers (conditions apply)

- Already pension le rahe log

- Non-residents

Scheme targeted hai un logon ke liye jinke paas koi safety system nahi hai.

APY Me Kitni Pension Milti Hai?

Ye wo section hai jahan maximum log galti kar dete hain. Unhe lagta hai ki APY ek investment scheme hai jahan paisa grow karega. Reality: APY ek fixed pension scheme hai, jahan aapko jo amount choose karte ho, wahi retirement ke baad milega — na kam, na zyada.

Sabse important baat ye hai ki yahan return se zyada timing matter karti hai. Agar aap early age me join karte ho, to same pension ke liye aapko bahut kam paisa dena padta hai. Late entry ka matlab hai same benefit ke liye zyada contribution.

Ayushman card Ki Eligibility kaise Check Kare…Read Here

₹1000, ₹2000, ₹3000, ₹4000, ₹5000 Plans Ka Breakdown

APY me aapko 5 fixed pension options milte hain, jisme aap apni capacity ke hisaab se choose kar sakte ho:

- ₹1000 per month pension

- ₹2000 per month pension

- ₹3000 per month pension

- ₹4000 per month pension

- ₹5000 per month pension

Zyada pension choose karna smart decision tabhi hai jab aap long-term contribution consistently kar pao. Warna beech me plan break hone ka risk badh jata hai.

Contribution vs Pension Comparison

Is scheme ka core logic simple hai:

- Early join = low contribution + same pension

- Late join = high contribution + same pension

Matlab system aapko reward karta hai agar aap jaldi start karte ho.

APY me profit ya return ka game nahi hai, yahan consistency aur timing hi sab kuch hai. Agar aap delay karte ho, to aapko zyada paisa dena padega bina extra benefit ke.

Real Example (Age 18, 25, 30 Cases)

Same ₹5000 pension ke liye alag age par contribution ka difference dekho:

- Age 18: ~₹210 per month

- Age 25: ~₹376 per month

- Age 30: ~₹577 per month

Sirf 12 saal delay karne par contribution almost 3x ho jata hai. Iska matlab simple hai: APY me sabse bada advantage paisa nahi, timing hai

Atal Pension Yojana Contribution Chart

Yahan se actual decision start hota hai. Zyada log sirf pension amount dekhkar plan choose kar lete hain ,lekin real game contribution ka hai.

Agar aapne apni monthly capacity aur long-term consistency ko ignore kiya, to plan fail ho sakta hai. Isliye pehle samjho: kitna dena padega aur kitne time tak dena padega.

Monthly Kitna Paisa Dena Padega

APY me aapko har month ek fixed amount contribute karna hota hai jo aapki:

- Age

- Selected pension plan

par depend karta hai.

- 18 saal ki age par ₹5000 plan = ~₹210/month

- 30 saal ki age par same plan = ~₹577/month

Amount chhota lagta hai, lekin long-term discipline maintain karna sabse tough part hota hai.

Age ke Hisaab se Contribution Kaise Change Hota Hai

Yahan sabse important rule samjho: Jitni late entry, utna zyada contribution

- Early join karoge → kam paisa dena padega

- Late join karoge → same benefit ke liye zyada paisa dena padega

APY me earning ka game nahi, timing ka game hai

| Age | ₹1000 Pension | ₹2000 Pension | ₹3000 Pension | ₹4000 Pension | ₹5000 Pension |

| 18 | ₹42 | ₹84 | ₹126 | ₹168 | ₹210 |

| 20 | ₹50 | ₹100 | ₹150 | ₹198 | ₹248 |

| 25 | ₹76 | ₹151 | ₹226 | ₹301 | ₹376 |

| 30 | ₹116 | ₹231 | ₹347 | ₹462 | ₹577 |

| 35 | ₹181 | ₹362 | ₹543 | ₹722 | ₹902 |

Atal Pension Yojana Me Apply Kaise Kare? (Online + Offline)

Yahan par log sabse badi galti karte hain — apply kar dete hain bina process samjhe. Result?

- Wrong auto-debit setup

- Contribution failure

- Account inactive

APY me entry easy hai, lekin exit ya correction mushkil ho sakta hai. Isliye start hi sahi karo.

Bank/Post Office se Apply Process

Ye sabse reliable aur safe method maana jata hai, especially un logon ke liye jo online process me comfortable nahi hain.

Step-by-step process:

- Nearest bank branch ya post office visit karo

- APY registration form lo

- Basic details fill karo (name, age, nominee, pension plan)

- Bank account details verify karvao

- Auto-debit mandate activate karvao

- Form submit karke acknowledgement le lo

Bank staff kai baar default plan select kar dete hain, form fill karte waqt apna pension plan khud verify karo.Form submit karne ke baad SMS confirmation check karna mandatory hai, warna aapko pata hi nahi chalega ki account active hua ya nahi.

Online Apply Ka Step-by-Step Process

Agar aap digital user ho, to online apply fastest method hai — lekin yahan accuracy important hai.

- Net banking / mobile banking login karo

- “Social Security Schemes” ya “APY” section open karo

- APY enrollment option select karo

- Personal details auto-fill verify karo

- Pension amount choose karo (₹1000–₹5000)

- Nominee details add karo

- Auto-debit consent confirm karo

- Submit karke confirmation download/save karo

Online process me ek chhoti si mistake (jaise wrong DOB ya nominee) future me correction headache ban sakti hai.

APY Account Me Contribution Kaise Jama Hota Hai?

Yahan sabse bada confusion hota hai. Log sochte hain ki APY me unhe manually paisa jama karna padega ,lekin reality bilkul alag hai.

APY ek auto-debit based system par kaam karta hai. Matlab aapko har mahine yaad rakhne ki zarurat nahi, lekin ek chhoti si galti (low balance) poore plan ko disturb kar sakti hai. APY me problem entry par nahi, consistency maintain karne me aati hai.

Auto-debit System Kaise Kaam Karta Hai

Jab aap APY join karte ho, tab aapka bank account scheme se link ho jata hai. Uske baad:

- Har month ek fixed date par paisa automatically deduct hota hai

- Aapko manually payment karne ki zarurat nahi hoti

- Contribution direct APY account me credit ho jata hai

Agar aapka contribution ₹376/month hai, to har mahine bank se automatically deduct ho jayega. System automatic hai, lekin responsibility aapki hai — account me balance maintain karna aapki duty hai.

Late Payment Penalty Kitni Lagti Hai

Agar auto-debit fail hota hai, to penalty lagti hai — jo chhoti lagti hai, lekin long-term me impact karti hai.

Penalty structure:

- ₹1/month → contribution up to ₹100

- ₹2/month → ₹101–₹500

- ₹5/month → ₹501–₹1000

- ₹10/month → above ₹1000

Penalty amount chhota hai, lekin repeated failure se account inactive ho sakta hai. Penalty problem nahi hai — habit problem hai. Jo log regular balance maintain nahi karte, unka plan automatically weak ho jata hai.

Contribution Miss Hone Par Kya Hoga

Yahan sabse bada risk hidden hai, jo log ignore kar dete hain. Agar aapka contribution regularly miss hota hai, to:

- Penalty lagti rahegi

- Account temporarily inactive ho sakta hai

- Long gap hone par account freeze ho sakta hai

- Extreme case me account close bhi ho sakta hai

APY Withdrawal Rules Aur Exit Policy

Yeh wo section hai jise log ignore kar dete hain — aur baad me regret karte hain. APY join karna easy hai, lekin paise nikalna itna flexible nahi hai.

APY ek long-term commitment hai, jahan entry simple hai lekin exit restricted hai. Ye scheme aapko freedom nahi deti, ye aapko discipline me baandh deti hai.

60 Saal Ke Baad Kya Milega

Jab aap 60 saal ke ho jate hain, tab APY ka main benefit start hota hai:

- Aapko fixed monthly pension milni start ho jati hai

- Pension amount wahi hota hai jo aapne plan choose kiya tha (₹1000–₹5000)

- Ye pension lifetime milti hai

Aapke baad (death ke baad) same pension aapke spouse ko milti hai . Yeh scheme ek tarah ka lifetime income system create karti hai — lekin amount fixed hota hai, increase nahi hota

Early Exit Allowed Hai Ya Nahi

Yahan sabse zyada confusion hota hai.

- 60 saal se pehle exit allowed nahi hota

- Serious illness

- Death

- Sirf aapka contribution + interest milega

- Government ka contribution (agar applicable) nahi milega

APY ko short-term investment samajhkar join karna sabse badi galti hai. Agar aapko flexibility chahiye, to APY aapke liye sahi option nahi hai

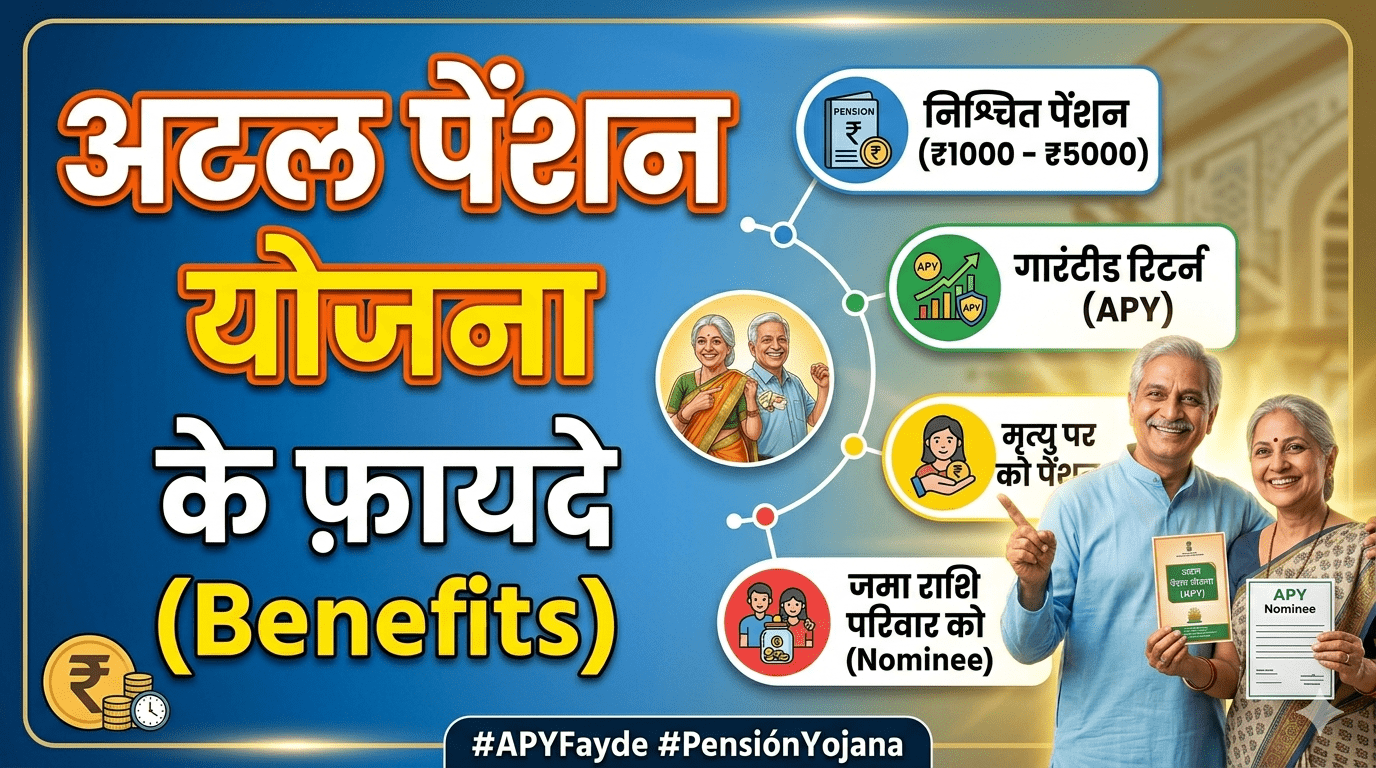

Death Ke Baad Nominee Ko Kya Benefit Milega

APY me family security ka element bhi include hai:

- Subscriber ki death ke baad → spouse ko same pension milti hai

- Spouse ki death ke baad → nominee ko corpus amount milta hai

APY sirf individual plan nahi hai — ye family protection plan bhi hai. Nominee details galat ya update nahi hui to future me claim issue aa sakta hai

Atal Pension Yojana Ke Fayde (Benefits)

APY ko samajhne ke liye sirf features dekhna enough nahi hai, real fayda tab samajh aata hai jab aap isse long-term perspective se dekhte ho.

Ye scheme flashy returns nahi deti, lekin ek cheez deti hai jo India me rare hai — guaranteed financial stability after retirement.. APY ka sabse bada benefit paisa nahi, peace of mind hai.

Guaranteed Pension Ka Advantage

APY ka sabse strong point hai iska guaranteed pension system.

- Aap jo plan choose karte ho (₹1000–₹5000), wahi amount aapko milega

- Market ups & downs ka koi effect nahi hota

- Pension lifetime fix rehti hai

Jahan doosri schemes me return uncertain hota hai, APY me certainty milti hai. Ye scheme un logon ke liye best hai jo risk nahi lena chahte aur minimum income secure karna chahte hain

Low Investment, Long-Term Security

APY ka entry cost bahut low hai — aap chhote amount se start kar sakte ho:

- ₹100–₹500 per month se bhi plan possible hai

- Long-term me ye ek stable income stream ban jata hai

Chhota investment ignore karna easy hota hai, lekin long-term me ye hi financial cushion ban jata hai. APY ka real power compounding nahi, consistency hai. Jo log regular payment karte hain, wo hi benefit le pate hain

Tax Benefits (Section 80CCD)

APY me contribution par aapko tax benefit bhi mil sakta hai:

- Section 80CCD(1) ke under deduction available hai

- Ye aapki taxable income ko reduce karta hai

Tax benefit secondary advantage hai, main focus pension security hona chahiye. Log tax saving ke liye join karte hain, lekin APY ka real value retirement protection hai

Ayushman Bharat Ki Eligibility Kaise Check Kare Read

APY Ke Nuksan (Drawbacks – Honest Section)

Har scheme ki tarah APY ke bhi kuch limitations hain, aur yahi wo part hai jo aksar bataya nahi jata. Agar aap sirf benefits dekhkar decision lete ho, to future me disappointment ho sakta hai.

APY safe hai, lekin perfect nahi hai. Jo scheme aapko guarantee deti hai, wo aapki flexibility aur growth ko limit bhi karti hai.

Fixed Return vs Inflation Problem

APY me jo pension aap choose karte ho, wo fixed rehti hai — lifetime tak change nahi hoti.

- ₹5000 aaj valuable lagta hai

- Lekin 20–30 saal baad uski value kaafi kam ho sakti hai

Aaj ₹5000 me jo kharcha hota hai, future me wahi cheez ₹10,000–₹15,000 tak pahunch sakti hai. APY inflation ko beat nahi karti — ye sirf minimum survival income provide karti hai. Agar aap sirf APY par depend karte ho, to retirement me financial gap aa sakta hai

Liquidity Issue (Paise Locked Rehte Hain)

APY ek long-term locked scheme hai:

- 60 saal se pehle paise nikalna almost impossible hai

- Emergency me bhi limited options hote hain

Aapka paisa locked rehta hai, chahe aapko urgent need hi kyu na ho. APY aapko saving discipline sikhata hai, lekin financial flexibility kam kar deta hai. Log apni emergency fund ke bina APY join kar lete hain — jo risky hai

Private Investment Options Se Comparison

Agar aap APY ko private options se compare karte ho (NPS, Mutual Funds, PPF), to difference clear ho jata hai:

- APY → Safe but low return

- Mutual Funds → High return but risk

- NPS → Balanced approach

APY wealth create nahi karta, ye sirf safety provide karta hai. Smart investors APY ko primary investment nahi banate, balki backup layer ke roop me use karte hain

APY vs NPS vs PPF – Kaunsa Better Hai?

Agar aap “best retirement plan” dhoond rahe hain, to sabse pehle ek baat clear kar lo. APY, NPS aur PPF ek dusre ke alternative nahi hain, ye alag purpose serve karte hain. Yahi reason hai ki log confuse hote hain aur galat decision le lete hain.

Risk vs Return Comparison

Retirement planning me sabse pehla decision hota hai, aap risk kitna le sakte ho aur return kitna chahte

| Scheme | Risk Level | Return Type | Stability | Growth Potential |

| APY | Zero Risk | Fixed Pension | High | Low |

| NPS | Medium Risk | Market Linked | Medium | High |

| PPF | Low Risk | Fixed Interest | High | Medium |

Jitna aap risk avoid karte ho, utna hi aap long-term growth miss karte ho

Kiske Liye Kaunsa Best Hai

Har scheme ka ek specific target user hota hai.

APY best hai agar

- Aap informal sector me ho

- Aapke paas pension nahi hai

- Aap guaranteed income chahte ho

NPS best hai agar

- Aap salaried ya self-employed ho

- Aap retirement ke liye corpus banana chahte ho

- Aap long-term invest kar sakte ho

PPF best hai agar

- Aap risk-free saving chahte ho

- Aapko stable aur predictable return chahiye

- Aap tax saving ke liye invest kar rahe ho

APY necessity hai, NPS opportunity hai, PPF safety net hai

Kiske Liye Kaunsa Best Hai

Har scheme ka ek specific target user hota hai.

APY best hai agar

- Aap informal sector me ho

- Aapke paas pension nahi hai

- Aap guaranteed income chahte ho

NPS best hai agar

- Aap salaried ya self-employed ho

- Aap retirement ke liye corpus banana chahte ho

- Aap long-term invest kar sakte ho

PPF best hai agar

- Aap risk-free saving chahte ho

- Aapko stable aur predictable return chahiye

- Aap tax saving ke liye invest kar rahe ho

APY necessity hai, NPS opportunity hai, PPF safety net hai

Conclusion – Kya Aapko Atal Pension Yojana Lena Chahiye?

Atal Pension Yojana lena chahiye agar aap guaranteed retirement pension chahte hain aur koi existing pension plan nahi hai. Ye low-risk, fixed-income scheme hai. Lekin higher returns ke liye APY ko NPS ya PPF ke saath combine karna zaruri hai — sirf APY par depend rehna sufficient nahi hai.

Atal Pension Yojana Kya Hai? FAQ

Kya Atal Pension Yojana safe hai?

Haan, ye government-backed scheme hai jisme fixed pension guarantee hoti hai.

APY me kitni pension milti hai?

₹1000 se ₹5000 tak monthly pension milti hai, aapki contribution par depend karta hai.

Kya APY middle class ke liye useful hai?

Haan, especially unke liye jinke paas koi pension system nahi hai.